When does this bubble pop?

That’s the fun part about this specific market, it isn’t a bubble that can pop. The people that caused this issue had the money to buy the houses they did. This is just the new normal, and the best part about that is that house prices only ever go up!

Yay! I can’t wait until the absolute garbage dilapidated pile of shit in the worst parts of town and a flood zone go from 300k now to 500k or more! It’s going to be so fun to see houses that I’d never in a million years want to live in, sell for hundreds of thousands above what I could afford anyway.

The argument from asshats with no empathy used to be: so move to a LCOL area (ignoring that work cant be found there.) Well even ignoring the work issue, those dont exist anymore. The WFH “movement” gave people the freedom to move to those LCOL areas so now they aren’t low cost anymore.

I can’t even leave the expensive shit hole area I live in because everywhere else is too expensive with less job opportunities… The future is so fun!

/wrist.

I don’t know how accurate it might be but I heard of a theory recently for the US that the recent reversal where students will be required to repay their loans in full is going to tank the housing market because a large chunk of people from the very demographic that would normally be first-time buyers won’t be able to afford to buy. There were supposed to be a bunch of cascading effects from this, but I’m sorry I can’t remember further details now.

Loan repayments resumed yesterday for over 100 million Americans. Now there are a lot of different options especially their income-driven ‘SAVE’ plan which calculates repayments based on earnings. So for me who’s struggling between jobs, I don’t have to pay jack until they see reported income luckily.

But the housing market here in Midwest US doesn’t seem like it’s changing for the better anytime soon. Median Housing cost is like triple average yearly salary, and on top of that our taxes are just abhorrent.

20% down payment is ridiculous these days. For the median home of 370k that’s 74k you need to have lying around.

Double that for Canada

$2,172,613 ($1,586,224.75 USD) if you want a detached in the Vancouver area

Condos bring the average down as they only cost $816,356 ($596,021.52 USD) which is pretty affordable as far as housing is concerned around the city

Detached homes shouldn’t even exist in Vancouver metrocore anymore so, it makes sense to be a fortune

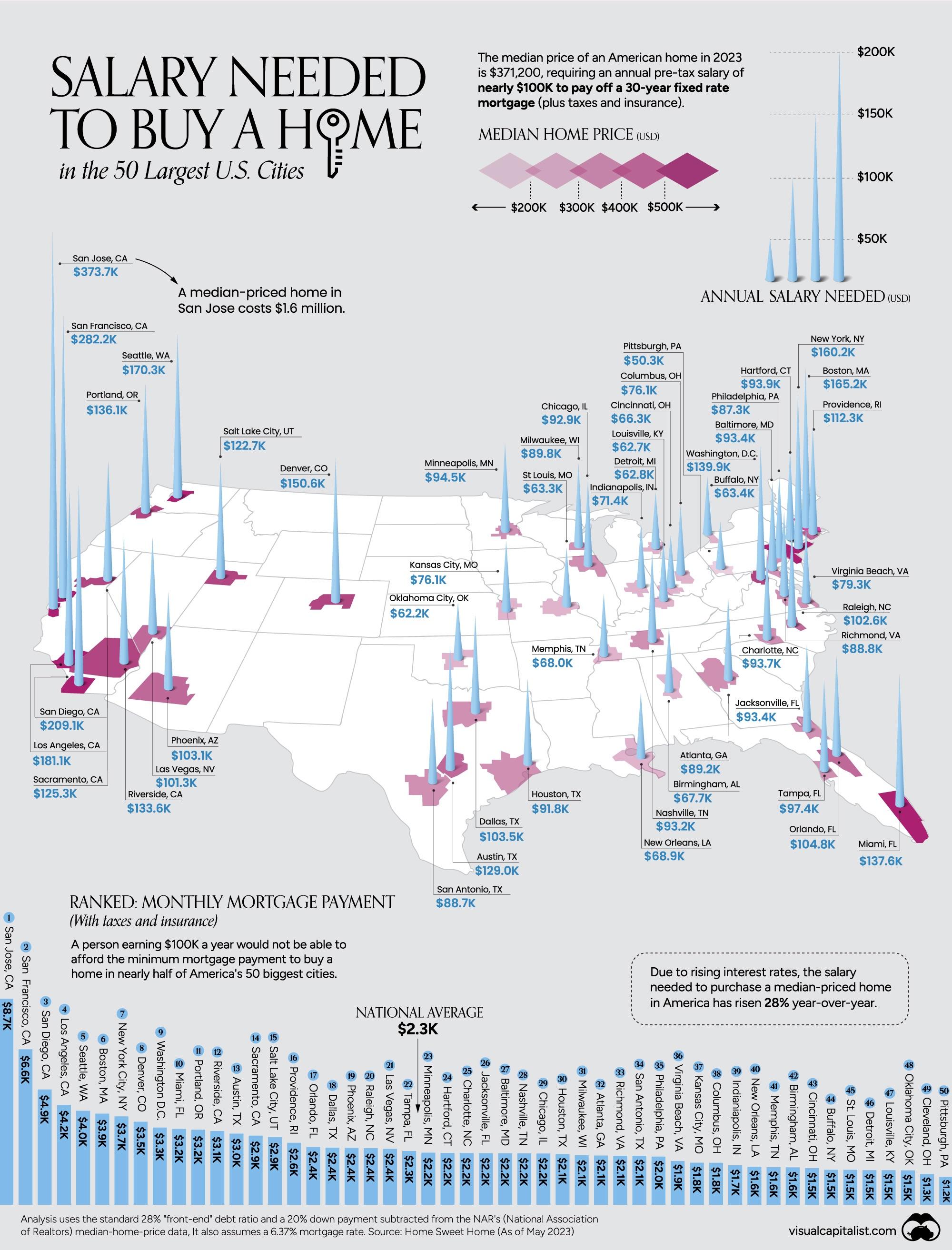

There must be something wrong with the math that they used here, because I’m familiar with a few of these markets and have a higher salary than what is listed and definetely couldn’t buy a house in those markets without it being more expensive than would be responsible - both in terms of down payment and monthly cost

For example, I think you’d need a lot more than 180k to buy a house in LA

It’s possible they’re including buyable apartments as well as single family houses but 180k still sounds WAY too low for LA

Yeah that could be it, or maybe they’re doing the math as literally “is your monthly take home less than the cost of the monthly payments”. In which case I could see 180 qualifying, but that isn’t how any sane person would define affordability lol

{kind=link}